Setting Up a Company in Brazil as a Foreigner: The 2026 Legal & Fiduciary Playbook for Foreign Founders, Investors, and Operators

Written by Luiz Duarte, a solicitor specialised in corporate and business law for fintechs and companies in the financial sector, and a founding partner of NDM Advogados.

Since 2014, we have been providing comprehensive legal advice to help tech companies grow safely and focus on what matters.

Updated on June, 16th 2026

Brazil’s massive consumer market and rapidly evolving digital ecosystem present unparalleled opportunities for global tech platforms, international investors, and innovative operators. However, setting up a company in Brazil, navigating the country’s complex legal, regulatory, and corporate frameworks can quickly become overwhelming for those arriving without a map. The old market adage remains true: Brazil is not for beginners, but it is highly rewarding for those who come prepared.

When establishing a corporate presence in Brazil, foreign founders frequently encounter a maze of conflicting advice regarding corporate structures, local representation, and tax obligations. This guide cuts through the noise, providing a straightforward blueprint for successfully launching your business. By understanding how to approach structural planning, asset protection, and local compliance, you can confidently turn administrative hurdles into a competitive advantage.

In practice, executing this playbook successfully requires a dual approach. You need sophisticated corporate and regulatory legal planning to draft the architecture, combined with dependable fiduciary infrastructure to handle day-to-day operational compliance. Let’s break down exactly what you need to know about setting up a company in Brazil as a foreigner.

The first strategic decision you will face is selecting the appropriate corporate vehicle for your Brazilian subsidiary. The vast majority of foreign enterprises choose either a Sociedade Limitada (LTDA) or a Sociedade Anônima (S.A.). While both offer limited liability protection for shareholders, their operational costs, compliance burdens, and corporate governance architectures differ significantly.

To help you assess which structure aligns best with your business model, growth projections, and capitalization strategy, we have compiled a structural comparison below.

| Feature | Sociedade Limitada (LTDA) | Sociedade Anônima (S.A.) |

| Governance Complexity | Low to Moderate. Governed by a simple Articles of Association (Contrato Social). | High. Requires a Board of Executive Directors; an optional Board of Directors (Conselho de Administração) is common for well funded startups. |

| Capital Structure | Divided into quotas. Less flexible for complex equity incentive plans (e.g., stock options). | Divided into shares. Highly flexible for issuing multiple share classes, vesting, and options. |

| Reporting & Publication | Minimal. Changes require simple amendments to be filed with the local Commercial Board (Junta Comercial). | High. Must publish financial statements and corporate resolutions publicly, increasing operational overhead. |

| Incorporation Timeline | Generally faster and less expensive to set up and maintain. | Longer setup timeline with higher structural maintenance fees. |

On the one hand, the LTDA is the ideal vehicle for early-stage market entry, service providers, or wholly-owned subsidiaries of foreign entities. It provides a lean, cost-efficient framework that shields the parent company while allowing operations to scale quickly. On the other hand, if your strategy involves raising local venture capital, issuing stock options to key local hires, or eventually pursuing a public listing, the S.A. is the standard requirement.

Actionable Insight: Do not over-engineer your initial market entry. Many foreign operators start as an LTDA to minimize corporate maintenance costs and later convert into an S.A. when institutional funding rounds or complex equity distributions require it.

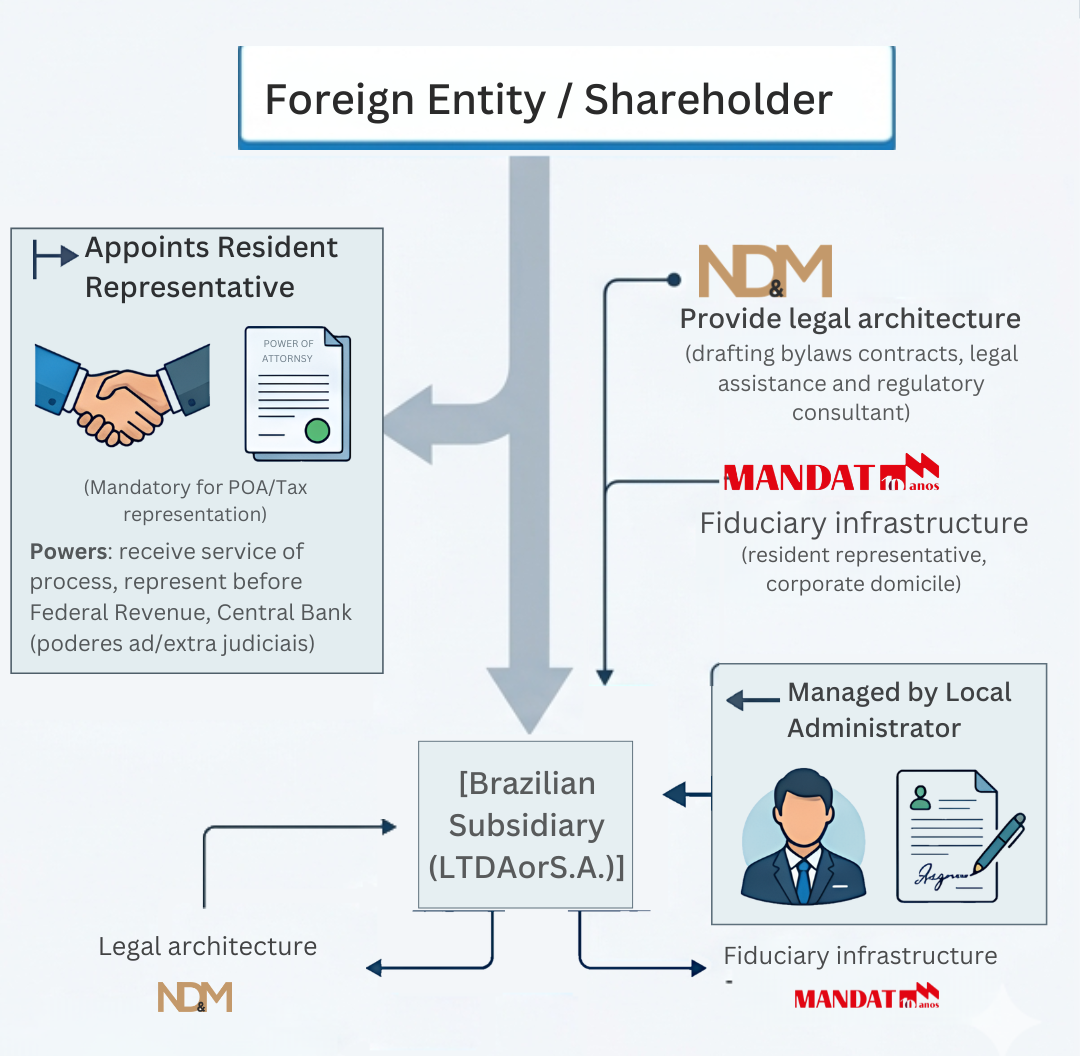

A common misconception is that a foreign individual or entity cannot own a Brazilian business without local partners. In reality, a Brazilian company can be 100% foreign-owned. However, the corporate and administrative “plumbing” requires strict adherence to mandatory fiduciary rules.

First, any foreign shareholder (whether an individual or a corporate entity) must obtain a taxpayer identification number in Brazil. For individuals, this is the CPF (Cadastro de Pessoas Físicas); for entities, it is the CNPJ (Cadastro Nacional da Pessoa Jurídica), registered through the Federal Revenue’s specialized systems, such as CADMTEC.

Second, because foreign shareholders reside outside the country’s jurisdiction, Brazilian corporate law dictates an absolute, non-negotiable requirement: they must appoint a resident representative via a formal Power of Attorney (POA). This POA must grant the representative specific powers to receive service of process (judicial notifications) on behalf of the foreign shareholder and to represent them before the Federal Revenue, the Central Bank, and municipal authorities (poderes ad/extrajudiciais).

Furthermore, the company itself must have a local Administrator who lives in Brazil. This individual holds the legal authority to sign contracts, open corporate bank accounts, and manage daily operations.

This is where the corporate puzzle pieces must fit together seamlessly:

Bringing capital into Brazil is not as simple as initiating a standard SWIFT wire transfer. To preserve your right to repatriate capital, pay dividends, or register future capital reductions without tax penalties, all inbound foreign investment must be registered with the Central Bank of Brazil (BACEN).

This capital flow is tracked through the Currency and Economic Financial Information System, specifically via the Foreign Direct Investment module (SCE-IED, formerly known as RDE-IED).

When transferring funds to your new Brazilian bank account, the transaction must follow a precise sequence:

Failing to register foreign capital properly or misclassifying incoming funds can trigger heavy administrative fines from BACEN, block future dividend distributions, or result in inbound funds being mischaracterized as taxable revenue rather than capital contributions.

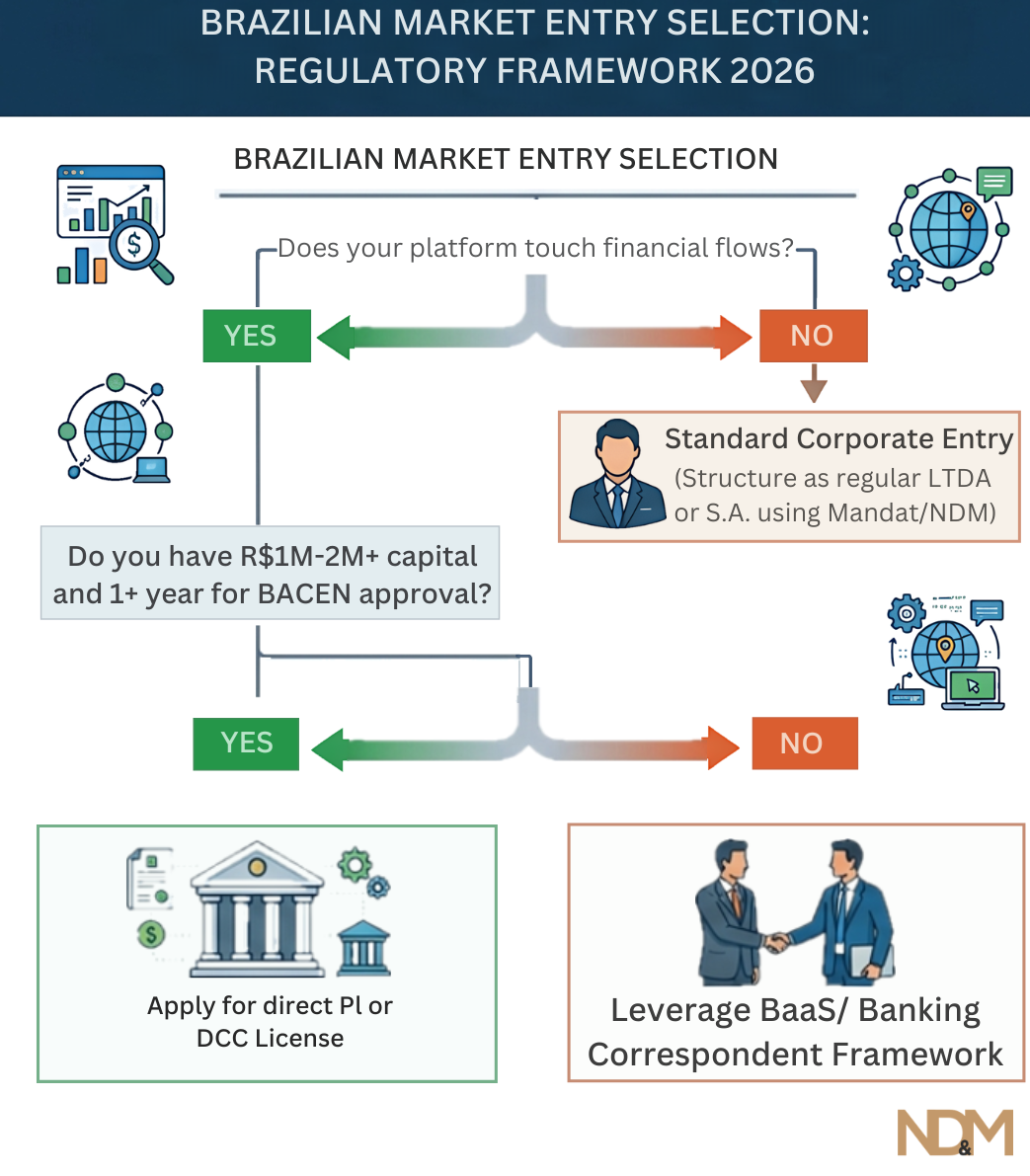

If your business operates in the financial technology, payments, or capital markets sectors, your legal roadmap requires an extra layer of scrutiny. The Central Bank of Brazil is widely recognized as one of the most innovative yet rigorous financial regulators in the world.

As detailed in NDM’s regulatory research, Brazil’s framework explicitly separates technology platforms from regulated financial activities. If your platform touches the movement of funds, payment processing, or credit origination, you must position yourself within one of BACEN’s approved frameworks:

In the current 2026 market environment, BACEN has transitioned from an era of purely encouraging new fintech entrants to one of strict, proactive supervision. Regulatory inspections are highly technical and heavily focused on data protection (LGPD) compliance, explainability of artificial intelligence in credit models, and robust Anti-Money Laundering and Counter-Terrorist Financing (AML/CFT) controls.

The Brazilian tax system is notoriously transactional, meaning that taxes are levied on gross revenues, financial transactions, and service flows, long before corporate profits are ever calculated. Additionally, cross-border service agreements face heavy withholding structures if not optimized correctly.

When establishing your company, you will generally select between two primary tax regimes:

On the human resources front, Brazil’s Consolidated Labor Laws (CLT) grant workers extensive statutory benefits, including a mandatory 13th-month salary, paid annual vacation with a 1/3 bonus, and a mandatory contribution to the severance fund (FGTS).

Many foreign tech startups make the critical mistake of hiring local developers or operators as independent contractors (PJ – Pessoa Jurídica) when their daily relationship features clear subordination, set hours, and habitual patterns. Brazilian labor courts frequently pierce these corporate veils, reclassifying contractors as traditional employees and imposing substantial retroactive liabilities on the parent organization.

Setting up a company in Brazil as a foreigner requires moving past the superficial advice to examine the actual plumbing of Brazilian corporate architecture. Success in this market is reserved for founders and investors who view legal compliance not as a bureaucratic box to check, but as a foundational asset for sustainable growth.

By coupling rigorous, tailored corporate design with compliant, local institutional representation, international businesses can completely neutralize regulatory friction. Establishing your entity correctly from day one protects your intellectual property, safeguards your global capitalization structure, and signals institutional maturity to local partners and clients alike.

Can a foreign company own 100% of a Brazilian company?

Yes. Brazilian corporate law allows local entities (LTDAs or S.As) to be entirely owned by foreign individuals or foreign legal entities. However, these foreign shareholders must maintain a resident representative in Brazil to handle corporate and tax obligations.

What is the role of a Resident Representative in Brazil?

The resident representative acts as a fiduciary link between the foreign shareholder and the Brazilian government. They hold a specific power of attorney to receive judicial service of process and represent the shareholder before tax and regulatory bodies. They do not automatically become a manager of the local company’s daily commercial operations unless explicitly appointed as an Administrator.

What happens if I fail to register foreign investment with the Central Bank?

Inbound funds not registered via the SCE-IED framework cannot be officially repatriated as return of capital, and you will face severe tax complications when attempting to remit dividends back to the parent company. Additionally, BACEN can apply administrative fines for non-compliance.

How long does it take to open a company in Brazil for a foreigner?

While a standard business for local residents can be opened in days, a company with foreign shareholders typically takes between 30 to 60 days. This timeline accounts for the time needed to legalize, translate, and apostille foreign corporate documents, obtain local tax IDs (CNPJ/CPF), and clear mandatory bank AML checks.

Estamos prontos para ajudar sua startup a crescer. Agende uma consulta e saiba mais!

Estamos prontos para ajudar seu negócio a crescer. Agende uma consulta e saiba mais!